September 2021

What was your month like?

If you’re a transactional professional – a class in which I include those who advise clients on the purchase and sale of businesses and investment assets, as well as those who assist clients in developing and implementing estate plans – it may be that the Earth’s 24-hour day, not to mention your own physical limitations, are preventing you from satisfying all your obligations as thoroughly and as quickly as you would like.[i]

Build Back Better

It is no secret that the surge in activity is attributable to the anxiety that many taxpayers – especially the owners of closely held businesses – and their advisers are experiencing following the decision by Congressional Democrats to pursue the President’s social programs (“Build Back Better”), and his plan to increase taxes, using the budget reconciliation process, thereby relegating the Republicans to the roles of observers and hecklers.

Under these circumstances, it was reasonable to think that the tax plan, announced by the White House in April and described in some detail by the Treasury in May, was on its way to being enacted. Consequently, business owners sought to close “strategic” deals or to complete transfers of property as soon as reasonably possible, and certainly before the then (and still) unknowable date of enactment which many believed would also be the effective date for many of the changes to be legislated.

Ways and Means

The release by the House Ways and Means Committee, in mid-September, of its proposed changes to the Code only increased the sense of urgency among taxpayers because several provisions were slated to become effective on the date of enactment, while other changes – including the tax increase on individuals with long-term capital gains – have left taxpayers despairing because they were to be applied retroactively.[ii]

In New York, where the income tax rates for individuals and corporations were substantially increased earlier in the year,[iii] the prospect of the anticipated federal tax increases has loomed especially large.

In fact, many business owners in the Empire State are considering whether to move their business and their residence to a lower-tax state – after all, it’s relatively easier to reduce state and local tax than the federal tax, using just your feet.[iv]

Are these the consequences intended by a rational tax policy? How did we get here?

Scorecard?

In August, Senator Manchin voted in favor of the $3.5 trillion reconciliation budget resolution that – if we are to believe his many statements since – he never supported.

Indeed, Senator Machin revealed last week that he had informed Senate Majority Leader Schumer in writing, the month before the vote, that he would not support any budget over $1.5 trillion.

Yet Senator Schumer was not dissuaded from bringing the resolution to the Senate floor for a vote and Senator Manchin was not disturbed about voting for the resolution. How does one reconcile these positions?

Who’s on First?

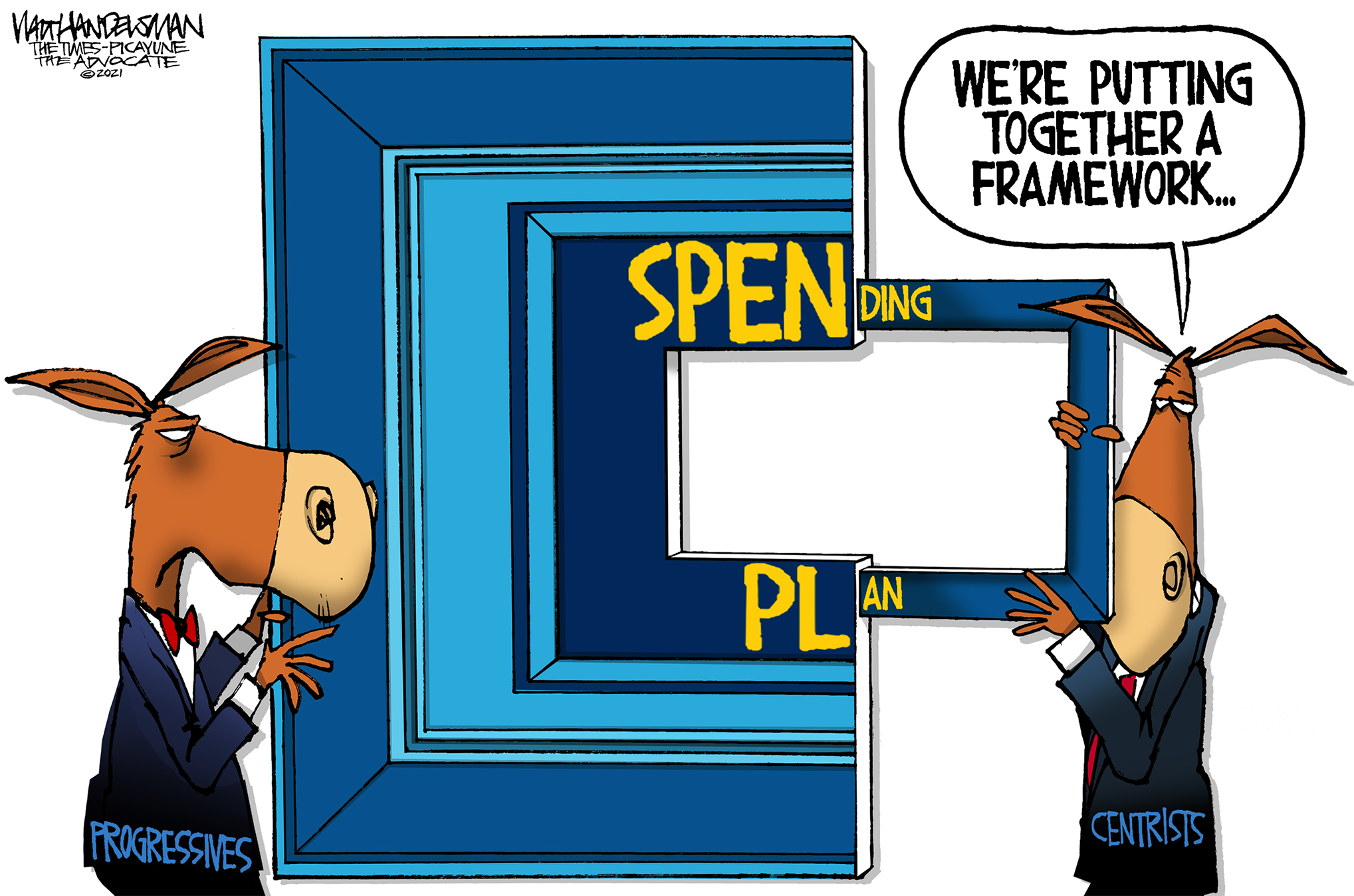

Regardless, following the passage of the resolution by both the Senate and the House,[v] committees from each Chamber were tasked with drafting legislation to implement the budget resolution.

The House Ways and Means Committee approved a $2.1 trillion tax bill that would fund much of the $3.5 trillion in expenditures proposed in the resolution.[vi] This tax bill – which omitted some of the President’s proposed tax changes, including a doubling of the tax rate on long-term capital gains and the elimination of the basis step-up at death – was quickly approved by the House Budget Committee last Saturday, following which it was sent to the House Rules Committee – its last stop before a vote on the House floor.

The White House expressed its disappointment with the tax bill, observing that the proposed tax increases were inadequate, and reaching out to legislators to generate support for more aggressive tax measures.[vii]

Following one of several meetings at the White House with the President and Speaker Pelosi, Senator Schumer announced that the Democratic leadership had agreed to a tax plan that would be based upon the Ways and Means bill but that would also include various additions to be made by the Senate.[viii]

Shortly thereafter, Speaker Pelosi stated that she hoped to bring the $3.5 trillion budget bill and the $1.2 trillion Senate-passed infrastructure/public works bill to a vote last week.

However, her more “progressive” colleagues in the House threatened to vote against the infrastructure measure unless Senators Manchin and Sinema[ix] first agreed to support the $3.5 trillion Build Back Better budget.

An Opening?

In the meantime, President Biden sought to convince Senators Manchin and Sinema to support his budget; his efforts included one-on-one meetings at the White House.

The President appears to have failed because, last Thursday, Sen. Manchin announced publicly that he would not support a budget that called for more than $1.5 trillion in spending.

However, the Senator also added that he wanted to reverse the changes made by the Republican-enacted Tax Cuts and Jobs Act.[x] In other words, the Senator probably supports many, but not all, of the tax changes in the Ways and Means bill.

What ensued was some unprofessional behavior among members of the moderate and progressive wings of the Democratic Party.

Not surprisingly, Speaker Pelosi decided against bringing the infrastructure bill to a vote, stating that she would wait until she was certain the Senate would go along with the President’s budget.

Now, Now Children

The next day, Friday, President Biden visited with Congressional Democrats on Capitol Hill, apparently to mediate between the progressives and the moderates of his Party; he is said to have encouraged them to adjust their expectations and to seek a compromise.[xi]

Following this meeting, and to the disappointment of many in his Party, the President told reporters he had no specific timeline for passing the infrastructure bill.

One day later, Speaker Pelosi acknowledged that the House needs more time before it can pass the “Build Back Better” budget; in other words, more time is needed to convince Senator Manchin to drop his objections. However, she also announced her goal to pass the infrastructure bill by the end of this month.[xii]

A New Approach?

What strategy will the Democratic leadership adopt during this period? It appears the White House and its allies will try to draw attention away from the cost of their social programs. According to one news source, “The administration argues that the Democratic-only reconciliation bill essentially won’t cost anything since the legislation, which could be as high as $3.5 trillion but is in flux, will be offset by tax increases on corporations and wealthy Americans.”[xiii]

And today, Sunday, on CNN’s “State of the Union,” Rep. Jayapal said she was confident both bills would pass. When asked about the cost of the proposed budget, she replied that her focus was on the delivery of social programs rather than their cost. “We will figure out the actual cost,” she said in what may be described as a conciliatory tone. When asked about Senator Manchin’s proposed $1.5 trillion cap, she replied that it was inadequate, but she did not yet have a counteroffer.

What’s Next?

What do we know?

Senator Manchin voted for a budget resolution, the spending provisions of which he does not fully support, but the tax provisions of which he does not necessarily oppose.

What, then, does the Senator from coal-dependent West Virginia[xiv] and Chair of the Senate Energy Committee want, other than a budget that calls for less than $3.5 trillion of spending, before he decides to vote in favor of the budget?

He hasn’t said yet, but would you be surprised if the Senator broached the subject of the President’s clean energy and climate change goals; specifically, the assistance to “energy transition” communities provided under the budget, which certainly includes West Virginia, the second-poorest state in the Union?[xv] I don’t think I’d fall off my chair.

When will he tells us, though? It’s not clear but, given what may have been overtures from the Administration and progressives in the House over the last couple of days, it may be soon.

When the Senator starts negotiating[xvi] – and we must assume that he will – query what it will mean for the income taxes, and for the gift and estate taxes, that will become payable by so many businesses and business owners.

I’m thinking the negotiations will have little-to-no impact from a substantive perspective – the tax increases and other tax-related changes proposed by Ways and Means will probably remain intact, and the Senate’s expected input may even amplify their effect.

Effective Date?

The effective date of these provisions, however, may be a different matter altogether – one can only hope that the longer it takes to reach an agreement on the budget, and the later in the current year that it is enacted, the greater is the possibility for the effective date to be deferred[xvii] into 2022. Much may depend upon what Senator Manchin has on his wish list.

The question of the effective date is no small thing. For example, the Ways and Means Committee’s bill provides that the increased individual rate for long-term capital gains (25 percent) will apply to gain recognized after September 13, 2021, which is the date on which the Committee’s bill was made public.[xviii]

The 50 percent reduction in the amount of gain that may be excluded from gross income on the sale of Section 1202 stock is to be effective for sales occurring after September 13, 2021.[xix]

Likewise, the Committee’s proposed changes relating to the use of grantor trusts by taxpayers in connection with estate planning[xx] would apply to trusts created on or after the date of enactment, and to that portion of an existing grantor trust that is attributable to a contribution made on or after such date.[xxi]

What to Do?

The passage of the budget resolution in August – almost four months after the White House announced its Build Back Better plan – manifested Congress’s intent to carry out the President’s tax plan.[xxii]

As indicated above, the passage of the resolution unleashed a flurry of taxpayer activity, some of which was anticipated, like the sale of assets ahead of an increase in tax rates.

The release of the Ways and Means bill just three weeks later, with the day after the release date as the effective date for the tax hike on capital gains, does not seem to have persuaded taxpayers to slow down their efforts to close deals notwithstanding they may have missed the proverbial boat.[xxiii]

Indeed, it appears that many business owners believe, or hope, that the effective date may be pushed back to the later of the date of enactment – which remains up in the air – or into 2022.

This seems like a rational course of action for those owners who have already decided, for bona fide non-tax business reasons, to dispose of their business, and for those for whom the expected tax increases and other proposed changes[xxiv] have tipped the scales in favor of such a sale.

Of course, Ways and Means also proposed certain measures that were not part of the President’s plan, including the accelerated reduction (by 50 percent) of the gift/estate tax exclusion amount (effective for transfers on or after January 1, 2022),[xxv] and limitations on the use of grantor trusts.

This has accelerated the schedule for many taxpayers to reconsider aspects of their plans for estate and gift taxes, including the use of their remaining exemption amount before the yearend, and the completion of any transactions involving the use of grantor trusts, including GRATs and sales to IDGTs, ahead of the still unknowable enactment/effective date.

As in the case of the capital gains rate hike, it is possible that the effective date for the changes to the grantor trust rules may be pushed back to the later of the date of enactment or, if the enactment date is much later in the year, into 2022.

In any case, it will behoove us to keep abreast of what Senator Manchin is doing. Although he is no friend of lower taxes, his agenda for what I believe are his own parochial interests may delay the enactment of the budget and thereby produce a more palatable effective date for legislation that is blatantly against the interests of the closely held business and its owners.

[i] It wouldn’t be much better on Mars, with its 25-hour day, but query whether its lower surface gravity would eliminate some of your sluggishness. The next closest planet, Venus, has a day of 5,832 hours. (A litigator’s dream? We may want to suggest they move.) Head the other way? Jupiter’s day is less than half an Earth-day, and its surface gravity is more than double the Earth’s. “Fuggedaboutit!”

[ii] The President’s plan, you may recall, would make the increased capital gains rate effective after April 2021; more than five months ago. The House bill would apply the increase to gain recognized after September 13, 2021.

[iii] From a top individual rate of 8.82% to rates ranging from 9.65% to 10.9%. The NYC rate remained at 3.876%.

An increase in the estate tax rate (from 16% to 20%) was averted.

The corporate tax rate went from 6.5% to 7.25%. The NYC rate on corporations remained at 8.85%.

[iv] Then there’s the question of the SALT cap. Yes, almost half the states have enacted workarounds for pass-through entities (partnerships and S corporations) modeled on IRS Notice 2020-75.

[v] The Senate voted just before it went on summer recess; the House reconvened briefly during its recess just to vote.

[vi] Among other things, the bill would increase the individual ordinary income tax rate from 37% to 39.6%, increase the capital gains rate from 20% to 25%, expand the application of the 3.8% surtax on net investment income, introduce a new 3% surcharge on those with income over $5 million, reduce in half the exclusion of gain from the sale of “Section 1202 stock,” increase the corporate tax rate from 21% to 26.5%, eliminate many transfer techniques used to minimize gift taxes, and reduce the unified estate and gift tax exemption by 50%.

[vii] The Rules Committee is empowered to amend the bill before sending it to the floor.

[viii] Senator Wyden, who chairs the Finance Committee, is not shy about tax hikes.

It is expected that certain items from the President’s tax plan will be reintroduced by the Senate.

[ix] What’s the story with the first-term Senator from the state that gave us Goldwater and McCain? She is even more enigmatic than the West Virginian. She has said very little about what keeps her up at night, though she is said to have shared her concerns with Senator Schumer in August – regardless of whether that occurred before or after the vote on the $3.5 trillion budget resolution, the fact remains she voted in favor of the resolution from which she now withholds her support.

Is she holding out for whatever help she can get for the last place Diamondbacks?

Neither she nor Manchin is up for reelection next year.

[x] P.L.115-97, enacted via the reconciliation process in late 2017.

[xi] I suppose this was directed at the progressives. Thus far, they have demonstrated a “my way or the highway” approach to legislating, though they showed signs of flexibility this weekend.

[xii] https://www.speaker.gov/newsroom/10221. “It’s about time,” she says over and over. Is it about time she retired?

[xiii] “White House seeks to flip debate on agenda price tag,” The Hill, Oct. 3, 2021.

[xiv] https://ohiorivervalleyinstitute.org/an-energy-state-no-more/ .

“West Virginia, which generates nearly twice as much electricity as it consumes, relies on coal for 91% of its output. So, as coal goes, so does West Virginia’s status as an energy state, which for many West Virginians is as much an issue of identity as it is of economics. But the economics are the driving force and they are irresistible.”

Did you know that Queens, Brooklyn, and Long Island each have a population greater than West Virginia? The state was formed when pro-Union Virginians seceded from Virginia one month after the latter seceded from the Union.

[xv] President Biden’s climate change goals of 80% clean electricity and 50% economy-wide carbon emissions reductions by 2030 may be an issue, though the budget provides assistance to “energy and industrial transition communities, including coal, oil and gas, and nuclear transition communities.” Perhaps the amounts allotted are inadequate?

[xvi] Is he any different from the progressives at this point? He hasn’t shown his cards, while they have not, until now, accepted anyone else’s cards. The result is the same.

[xvii] Like the tax pun?

[xviii] https://www.taxslaw.com/2021/09/tax-hikes-effective-dates-and-selling-a-business/. I was involved in one transaction that “had” to close on Monday, September 13. We didn’t know that until the afternoon of Friday, September 10, following a “friendly” call to one of the parties. The Ways and Means bill was released around 11:30 pm on Sunday, the 12th. Call me naïve.

[xix] https://www.rivkinradler.com/publications/disposing-of-assets-under-the-ways-and-means-committees-proposals/.

[xx] https://www.taxslaw.com/2021/09/grantor-trusts-on-the-precipice/ .

[xxi] N.B. There have been whispers that this change will be applied to all grantor trusts, regardless of when formed or funded.

[xxii] Not to mention the spending plan.

I might add, this happened without hearings, without reports from interested persons and experts, without any input from the public – it happened because one political party wanted it.

WTF is that about? Wake up America. These career politicians (on either side of the aisle) are not Plato’s philosopher kings. Campaign reform? Definitely. Term limits? Time to think hard on this. This is interesting: https://www.periodicalpress.senate.gov/seniority/ and https://www.statista.com/chart/14506/who-are-the-longest-serving-representatives-in-the-house/ .

[xxiii] I have been consulting the “Dictionary of Idioms” given to me by a close friend.

[xxiv] For example, the new transaction bank reporting requirements that are being considered.

[xxv] Currently set to occur after 2025.